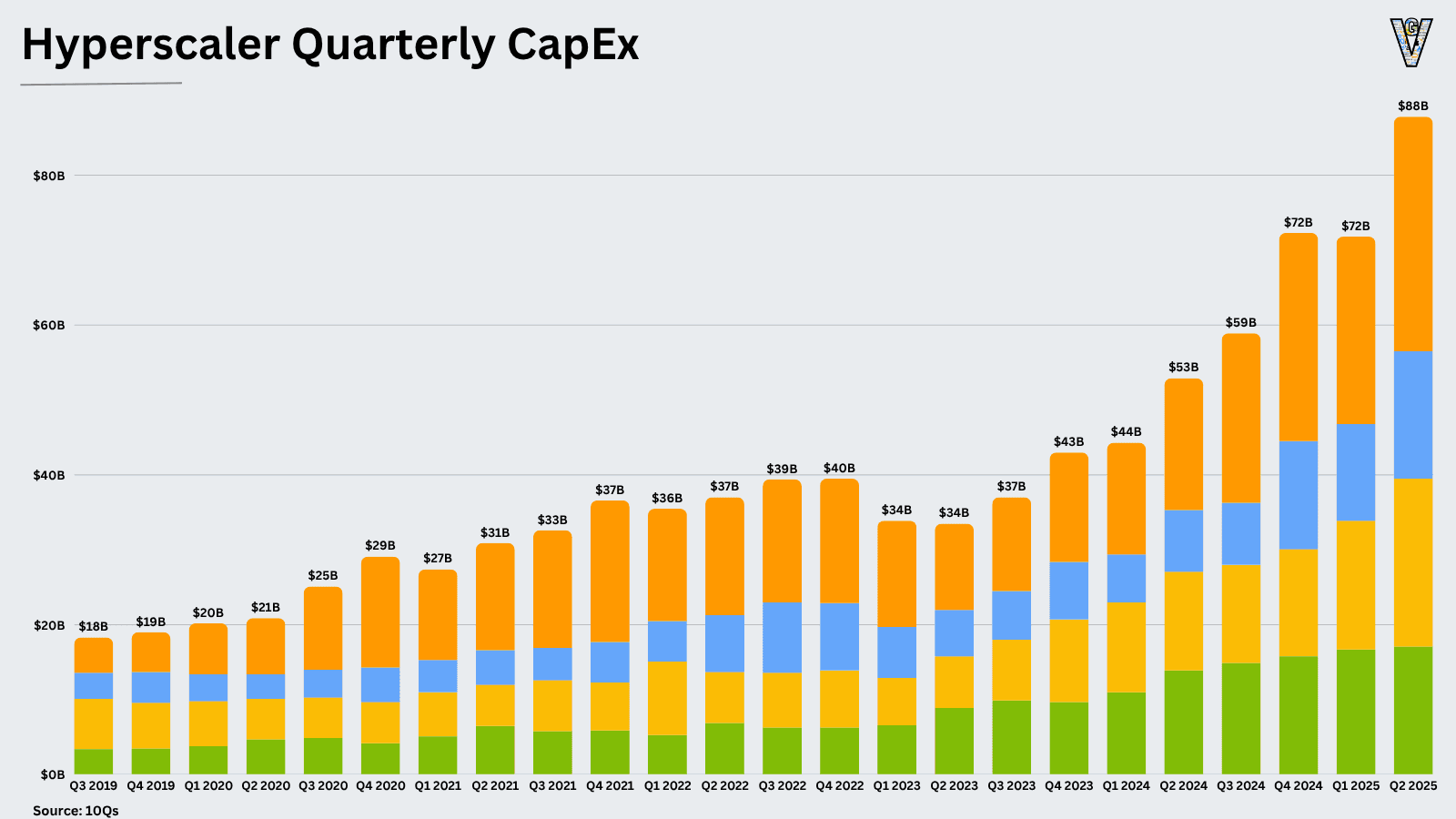

Morgan Stanley forecasts the top 5 cloud providers' total capex will hit $1.2 trillion next year. By 2028, that figure is expected to reach $1.4 trillion, with computing power quadrupling.

Key facts

- $1.2 trillion: top 5 cloud capex forecast for 2027.

- $1.4 trillion: projected capex by 2028.

- Computing power expected to quadruple by 2028.

- Google booked Intel to package 3 million TPUs.

- Google launched Gemini 2.0 with any-to-any multimodal models.

Morgan Stanley's analysts project the combined capital expenditure of the five largest cloud providers — Amazon Web Services, Microsoft Azure, Google Cloud, Oracle, and IBM — will surge to $1.2 trillion in 2027, up from an estimated ~$900 billion in 2026. By 2028, the bank expects that number to reach $1.4 trillion According to 36Kr. The accompanying forecast: computing power across these hyperscalers will roughly quadruple in the same timeframe.

Wall Street does not appear to view these outlays as reckless. The report's framing suggests investors are comfortable with the massive spend, seeing it as necessary to meet surging demand for AI training and inference workloads. This contrasts with historical capex cycles where such growth would have triggered margin concerns. The scale is staggering: $1.2 trillion is roughly the entire GDP of Australia, spent in a single year by just five companies on data centers, GPUs, networking, and power infrastructure.

The Structural Shift

This forecast underscores a deeper reality: AI infrastructure is becoming a utility-like capital sink, not a cyclical tech investment. The quadrupling of compute power — driven by clusters of Nvidia H100 and B200 GPUs, Google's TPU v6, and custom silicon from Amazon and Microsoft — implies a race to build out capacity before demand fully materializes. The risk is overbuild, but the bet is that inference demand, particularly from agentic AI systems, will absorb the supply.

For Google Cloud specifically, the projection aligns with its ongoing expansion. Google has booked Intel to package 3 million TPUs, and its recent launch of any-to-any multimodal models via Gemini 2.0 gives it a structural advantage in attracting AI-native workloads. But the capex burden is shared: Microsoft and Amazon are each spending tens of billions quarterly.

What This Means for AI Startups

The implication for AI companies like OpenAI and Anthropic is indirect but profound. If cloud compute becomes cheaper and more abundant, the cost of training frontier models drops, potentially accelerating the commoditization of foundation models. Conversely, startups that rely on exclusive cloud deals — like OpenAI with Microsoft — may find themselves locked into pricing that doesn't reflect the capex glut.

Morgan Stanley's report is a bet on demand elasticity: that cheaper compute will unlock new use cases, not just subsidize existing ones. If that bet is wrong, the industry faces a capex hangover. But for now, Wall Street is all in.

What to watch

Watch the Q3 2026 earnings calls from Amazon, Microsoft, and Google for actual capex guidance vs. Morgan Stanley's forecast. Any downward revision would signal softening demand; upward surprises would validate the $1.2 trillion target.

Source: news.google.com